- FnF abide by the Federal Housing Enterprises Financial Safety and Soundness Act of 1992.

- HERA is just a law to amend the Act of 1992 mentioned.

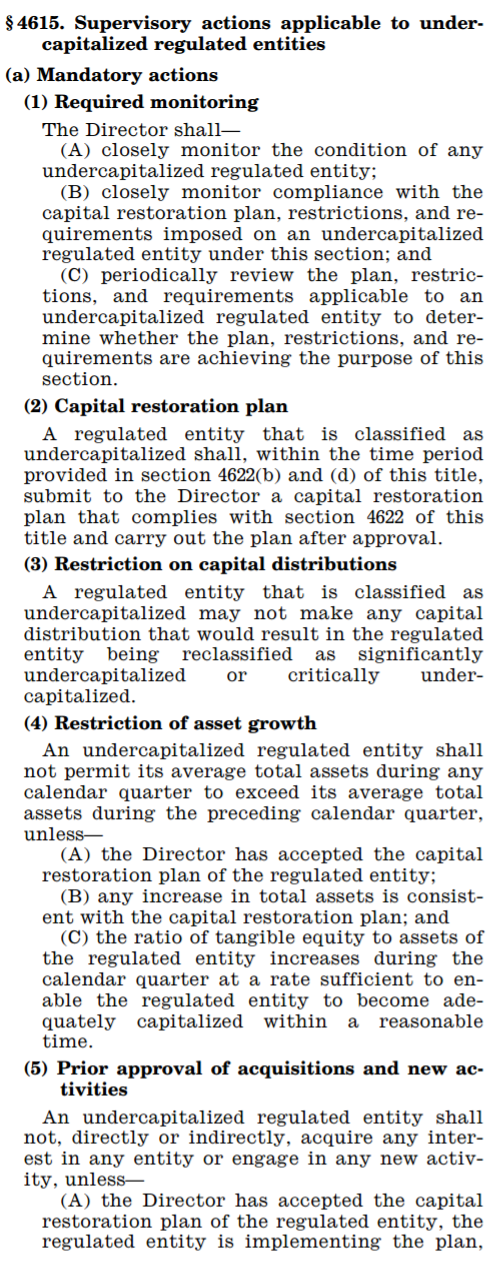

- FHFA hasn't complied with its duty of maintenance of adequate capital.

- FHFA hasn't complied with its duty of Capital classification disclosure for FnF.

- FHFA hasn't complied with its duty of Restriction of Capital Distribution to an undercapitalized FnF.

- FHFA hasn't complied with its duty of approving Capital Restoration Plan for FnF.

Fannie Mae and Freddie Mac still abide by the Financial Safety and Soundness Act of 1992. In July 2008, the Housing Economy Recovery Act (HERA) was enacted for the purpose to amend some aspects of the previous Law, but for the rest, the FSSA is still in place. In fact, if you read now the FSSA, the amendments approved in HERA are included.

For instance, one amendment of HERA was to change the name of the Act for Federal Housing Enterprises Financial Safety and Soundness Act of 1992 (see SEC. 1142). Or change the name "Enterprise" for "regulated entity".

Since the day the

Enterprises were put into Conservatorship, there have been a series of

agreements between the FHFA and Treasury that have erased their Capital

massively, and this is prohibited by Law because HERA (and thus FSSA) explicitly

says that the Director shall ensure the maintenance of adequate capital.

HERA. SEC. 1313. DUTIES AND AUTHORITIES OF DIRECTOR.‘‘(a) DUTIES.—‘‘(1) PRINCIPAL DUTIES.—The principal duties of the Director shall be—‘‘(B) to ensure that—‘‘(i) each regulated entity operates in a safe and sound manner, including maintenance of adequate capital and internal control

Therefore, all the

agreements between the FHFA and the Treasury or Congress’ actions that have erased

a substantial amount of capital from the Enterprises should be deemed voided

effective the day they were approved. This is what the FHFA's Director

should have done in order to abide by his duties under Law.

Recapitulation of

capital erosion and capital distribution agreements since Conservatorship began:

1. The Treasury

purchased $1 billion worth of Senior Preferred Stock in each Enterprise the day

of Conservatorship, without disbursing the cash, that is, for free, and the

justification was: "Initial Commitment Fee". But the reason has more

to do with the need to place the Enterprises under Conservatorship, because it

reduced the Core Capital by the same amount.

2. The day of

Conservatorship the government purchased a warrant representing 79.9% of the

common stock that made the common stock to plummet, which translates into huge capital

erosion.

3. The day of

Conservatorship the Enterprises agreed to pay a usurer 10% dividend to Treasury,

but their Congressional Charters already contemplated a bailout scheme that is

the central piece of the GSEs: Charter. SECTION 305 (c):

Each purchase of obligations by the Secretary of the Treasury under this subsection shall be upon terms and conditions established to yield a rate of return determined by the Secretary to be appropriate, taking into consideration the current average rate on outstanding marketable obligations of the United States as of the last day of the month preceding the making of the purchase.

And the 2 year Treasury note stayed

at 0.3% - 0.4% annual rate since long time ago. Thanks to this bailout scheme

the enterprises get funds on the market at low rates so that they can fulfill

their Countercyclical role.

4. The establishment

of a deferred tax asset valuation allowance, reduced capital by $21 billion for

Fannie Mae and $14 billion for Freddie Mac in 2008, also contributed to the

total capital erosion. Later the enterprises were allowed to build a DTA, but

due to the Net Worth Sweep that will be explained next, the Enterprises didn’t

benefit from these DTA.

5. Temporary

Payroll Tax Cut Continuation Act of 2011 requires the FHFA to direct the Enterprises

to raise the g-fees but the proceeds are sent to Treasury. This action violates

FnF’s Congressional Charters: "no fee or charge may be assessed or

collected by the United States".

The Federal

National Mortgage Association Charter Act [12 U.S.C. 1716 et seq.]

The Federal

Home Loan Mortgage Corporation Act [12 U.S.C. 1451 et seq.]

6. Net Worth Sweep since April 2012. The Net Worth amount is assets less liabilities. The amount remitted to Treasury each quarter as dividend is all the profits, calculated: Net Worth amount less the Applicable Capital Reserve amount ($600 million for 2017).

It's stunning that

a government doesn't allow to build capital above $600 million.

Under this 2012

Third Amendment of the Agreement with Treasury (SPSPA), the Applicable Capital

Reserve started at $3 billion for 2013, but it was set that it will be reduced

by an equal amount until $0 for 2018. Therefore the FHFA sets a lower Capital

Reserve target each year until it reaches zero in 2018, which is the opposite of what

the Law requires (Capital Restoration Plan).

The NWS also violates the Charters for the same reason laid out with the Temporary Payroll TCCA mentioned before.

The NWS also violates the Charters for the same reason laid out with the Temporary Payroll TCCA mentioned before.

7. During

Conservatorship, FnF have been issuing 30yr. callable zero coupon bonds, that soon

later have been redeemed at an outstanding high rate of return. Explained here.

8. Credit Risk Transfer transactions to reduce credit risk. FnF waive

revenues (and thus, earnings) when they initiated in 2013 the credit risk

transfers program because, in FHFA’s Director’s own words: “Like any kind

of insurance, the Enterprises must either pay a premium or forgo a portion of

their guarantee fee income”.

9. Sale of

reperforming modified loans. They are sold with a haircut because the buyer is

obliged to offer loss mitigation options to any borrower who may redefault, therefore,

the buyers aren’t paying the Unpaid Principal Balance for sure. It could be a

backdoor mortgage debt forgiveness plan.

9. Sale of

reperforming modified loans. They are sold with a haircut because the buyer is

obliged to offer loss mitigation options to any borrower who may redefault, therefore,

the buyers aren’t paying the Unpaid Principal Balance for sure. It could be a

backdoor mortgage debt forgiveness plan.

But their Congressional Charter doesn’t allow them to pay a fee for

insurance, but to engage in operations with mortgages or interest therein.

Again, FHFA can take any action but it can’t contravene the FHEFSSA of

1992 and their Charter because both are currently in force.

Even in the same speech at American Mortgage Conference, FHFA’s

Watt recognizes he isn’t complying with

FnF's business model written in the Charter, which is an unlawful act: “The Enterprises'

credit risk transfer programs are a significant departure from their prior

business model”.

Also, it can be deemed Capital distribution (Earnings is Capital) which

is prohibited for undercapitalized GSEs according to the Law of 1992.

Finally, it’s worth mentioning that this Credit Risk Transfers program doesn’t make economic sense, because they are implemented to mortgage loans with

maximum Loan-To-Value of 80%, which are the only loans that FnF can buy

according to their Charter. The loan needs to have mortgage insurance (bought

by the borrowers and paid for in their monthly payments) for loans with LTV

higher than 80%. And covering the credit risk of loans with 80% LTV ratio is insane because they

have a very low credit risk already, which translates into very low Serious

Delinquency rates.

For instance, Freddie Mac signaled in its latest report that

the Serious Delinquency rate for its Core single-family book (74% of portfolio) is just 0.19%, a

disproportionately low rate compared with the financial sector.

Finally, it’s worth

mentioning another section of FSSA. It requires the FHFA to establish CAPITAL

CLASSIFICATIONS (SEC. 1142), and guess what the FHFA did when Conservatorship

began: it suspended the capital classification disclosure for Fannie Mae and Freddie Mac.

This is because

HERA requires Prompt Corrective Actions (Subtitle C. Page 77) amending The Financial

Safety and Soundness Act of 1992 (12 U.S.C. 4613), and if we don't know the Capital Classification of FnF, there won't be pressure to approve Capital Restoration plans.

As always, everything is set forth in the Federal Housing

Enterprises Financial Safety and Soundness Act of 1992:

FIRST. It’s established the Minimum Capital Levels for the Enterprises:

THIRD. Supervisory

actions applicable to undercapitalized regulated entities and to significantly

undercapitalized regulated entities:

The FHFA's Directors neither read the Federal Housing

Enterprises Financial Safety and Soundness Act of 1992, nor the Enterprises' Congressional Charters, because they preferred to embark in a campaign of Capital Erosion, so that the Conservatorship continues forever and, in the meantime, banks, hedge-funds and the government make a lot of money off transactions using FnF's balance-sheet.

Unlike with FnF, the FHFA required

the FHLBs classified as undercapitalized to submit a capital restoration plan

for approval, execute the approved plan, suspend dividend payments and excess

stock redemptions or repurchases, and didn't permit growth of its average total

assets in any calendar quarter beyond the average total assets of the preceding

quarter, unless otherwise approved by the FHFA.

Maybe the FHFA and the Treasury thought that, because in HERA is only explained the Prompt Corrective Actions for the FHLBs, people would think that Fannie Mae and Freddie Mac are left apart. This is why many people close to the Hedge-funds and banks repeat continuously that FnF are under HERA, but they are not. What HERA did is just amend the Financial Safety and Soundness Act of 1992, therefore FnF are still under FSSA which sets forth the capital classifications and urges the FHFA to take measures to restore adequate capital levels in order to allow the Enterprises to operate in a safe and sound manner.

Maybe the FHFA and the Treasury thought that, because in HERA is only explained the Prompt Corrective Actions for the FHLBs, people would think that Fannie Mae and Freddie Mac are left apart. This is why many people close to the Hedge-funds and banks repeat continuously that FnF are under HERA, but they are not. What HERA did is just amend the Financial Safety and Soundness Act of 1992, therefore FnF are still under FSSA which sets forth the capital classifications and urges the FHFA to take measures to restore adequate capital levels in order to allow the Enterprises to operate in a safe and sound manner.

BOTTOM LINE

The FHFA violates the Federal Housing Enterprises Financial Safety and Soundness Act of 1992 because it has agreed or it hasn’t opposed to all the capital erosion actions we've seen since Conservatorship began and, secondly, because it hasn’t directed the Enterprises to take measures to have adequate capital.

FnF's common shareholders reserve the right to sue the FHFA and the U.S. government for the harm suffered.

Author?

ReplyDeleteIt's a personal blog.

DeleteFollow me on Twitter: https://twitter.com/CarlosVignote

ReplyDeleteRECAPITALIZATION PLAN:

ReplyDelete1. Release from Conservatorship.

2. Warrant cancelled.

3. NWS cancelled.

4. Temporary Payroll TCCA of 2011 repealed.

5. Sale of reperforming modified loans halted.

The ratio of Total Loan Loss Reserves to Annualized Net Charge-offs for single family homes stands at 8.2, according to Freddie Mac (it includes the reserve for TDR concessions and adjusted to take into account the prohibition to sell reperforming loans with a credit-loss)

OUTCOME: PER= 12 times, half the S&P500 Index

- FMCC: $195 pps

- FNMA: $135 pps

These are my assumptions. Do your due diligence.

Yes ...

DeleteThe Junior Preferred Shares' prospectus would be restated with a lower dividend yield to reflect the current market rates.

ReplyDeleteGreat analysis, I recommend reaching out to Fairholme and Perry with this. Also shoot it to WSJ (now that Carney is gone), FT, Bloomberg and Rolling Stone.

ReplyDeleteI've followed the GSEs for awhile and no one has covered the Federal Housing Enterprises Financial Safety and Soundness Act of 1992

LEGAL ADVICE

ReplyDeleteIf someone wants to start litigation, which I strongly recommend, here are the three steps in the legal defense:

1st. HERA has directed the Courts to not take any action against the Conservatorship by all means: "In their motions to dismiss defendants argue the Court lacks jurisdiction because HERA prohibits the relief sought in the Complaint. Specifically, 12 U.S.C. § 4617(f) states that "[e]xcept as provided in this section or at the request of the Director, no court may take any action to restrain or affect the exercise of powers or functions of the Agency as a conservator or a receiver,"" Page 18 http://www.glenbradford.com/wp-content/uploads/2016/11/16-02107-0063.pdf

The legal argument to rebut this is that the Conservatorship's actions can't go against the law (FHEFSSA of 1992) that regulates the functions of the FHFA as regulator of FnF and where this amendment of HERA is incorporated.

2nd. Copy/paste this article.

3rd. Direct your lawyer to file the lawsuit in the U.S. Court of Federal Claims in Washington. That court handles cases against the federal government.

Disclosure: I'm not a lawyer.

Hey Carlos! Amazing analysis. Thank you for examining and explaining this. I've been invested in FNMA for about 6 months now. What is your reasoning behind FMCC being worth significantly more than FNMA? I've never heard this argument before until now.

ReplyDeleteHere is why (data as of end of 1Q2017):

Delete1. Net Interest Income Yield (Difference of yields between assets and the cost of funding those assets):

FMCC: 0.76%

FNMA: 0.66%

2.Net Income in the Multifamily Business:

FMCC: $445 million

FNMA: $431 million

3. The third amendment of the SPSPA obliges the Enterprises to reduce their mortgage-related Investment Portfolio 15% each year to reach $250 billion by 2018. Now they are similar and going down, therefore, they have the same Investment Portfolio but FMCC has nearly half the amount of common shares outstanding than FNMA.

Also FMCC was much healthier than FNMA at the beginning of Conservatorship because Countrywide was FNMA's best client.

DeleteAll of this makes a smaller company like FMCC have similar earnings than FNMA.

Thank you Carlos! You make very good points. I appreciate your perspective and all that you have done. I look forward to future posts. Have a great day!!

DeleteI have updated the article in the section about the Credit Risk Transfers program (8) with more details after reading the Director of FHFA's speech at American Mortgage Conference on May 18th.

ReplyDeleteWE'VE GOT THE SMOKING GUN

ReplyDeleteIn two tweets or thread of tweets if you wish to read more:

1. https://twitter.com/CarlosVignote/status/870885150304989185

2. https://twitter.com/CarlosVignote/status/871237943972769792

Now is when you can file the lawsuit.

Here the FHFA says that "may" is "permissive rather than obligatory".

ReplyDeletehttp://gselinks.com/Court_Filings/Robinson/16-6680-0033.pdf

Wrong.